December 1, 2020 – Semi Wet Chemicals US$2B Market Threatened by Localization – Specialty Cleaning and Etching Changes Could Cause Yield Losses

November 16, 2020 – Wet Copper Deposition Materials for ICs and Packages – Steady growth in demand forecasted through 2024

November 5, 2020 – Refreshing Material Advances for Logic, Memory, and Packaging – 5th CMC Conference “After-Hours” Available up to December 11

October 21, 2020 – Critical Materials – PVD Targets US$1B and Growing Strong – Increasing demand forecasted through 2024

September 21, 2020 – Semiconductor Materials Market to Hit $50B in 2020 Up 3% – Winds Reverse on the Global Supply-Chain Seas

August 27, 2020 – CMP Consumables US$2.5B in 2020 for IC Fabs – Stable world-wide growth in demand forecasted through 2024

July 29, 2020 – Rare Earth Elements Supply Uncertain for IC Fabs – China’s de facto monopoly control remains for now

July 4, 2020 – Quartz Parts Market for Semiconductor Fabs Downward Trend Expected to US$1.2B – Skilled Labor Shortage for Quartz Tube Fabricator Concerns

July 1, 2020 – 2020 CMC Conference – State of the Art Virtual Engaging – 2020 CMC Conference – State of the Art Virtual Engaging

May 29, 2020 – CMC COVID-19 Impact Survey Shows Supply-Chain Strength – Pre-registrants for 2020 CMC Conference access COVID-19 Info

TNews2 – CMC Workshop Flags Looming Shortages of IPA and Sulfuric

March 9, 2020 – EUV Materials Small But Strategic Fraction of $1.6B IC Photoresists Market

TNews – Materials eBlast – Wet Chemicals & Specialty Cleans 2020 Q1

January 14, 2020 – Semiconductor Materials growing to nearly $50B Market in 2020 after Downturn

December 1, 2020

Semi Wet Chemicals US$2B Market Threatened by Localization

Specialty Cleaning and Etching Changes Could Cause Yield Losses

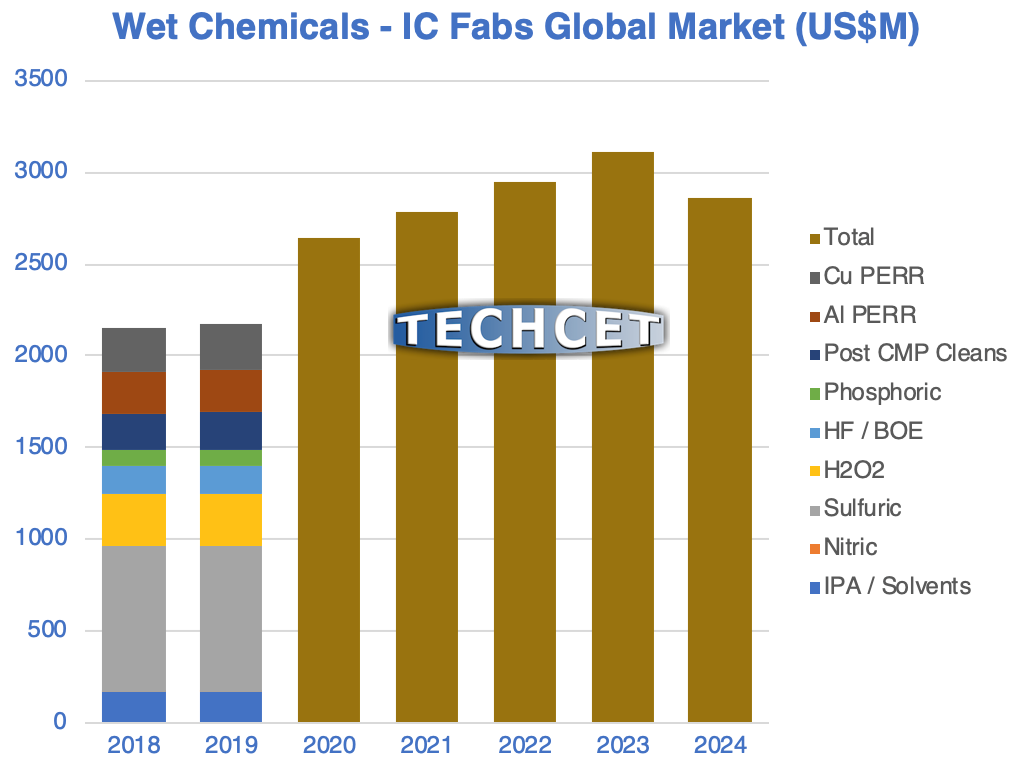

San Diego, CA, December 1, 2020: TECHCET—the electronic materials advisory firm providing business and technology information—announces the global market for wet chemicals needed for global semiconductor fabrication in 2021 is forecast to reach US$2 billion. However, recent trade wars threaten the stability of global supply-chains for critical materials, with China, the European Union, Japan, and the U.S. all announcing plans to create parallel local sources for electronic materials, and South Korea and Taiwan increasing investments in chemical production. There are many specialty blends needed as well as ultra-pure neat chemicals, and all are growing in demand as seen in the Figure (below) from the latest Critical Materials Report™ (CMR) quarterly update on Wet Chemicals & Specialty Cleans.

The most advanced IC fabs for logic and memory chips require purity levels in materials so extreme that trace contaminants below parts-per-billion can cause millions in dollars of commercial yield losses. When raw materials sources or refining processes change there are corresponding changes in the trace contaminants and the chemical fingerprint so semiconductor fabs require that suppliers use advanced metrology and sophisticated analytic methods to re-qualify any changes.

“Advanced commercial ICs can only be profitably fabricated when the critical materials supply-chain is locked in from the very beginning at the mine or other industrial feedstock,” explained Terry Francis, TECHCET Director of Technology and Senior Analyst and author of the report. “For anhydrous-HF supply, we’re seeing a shift in the fluorine source from fluorspar mining to alternates including FluoroSilicic Acid (FSA), depleted uranium hexafluoride, and aluminum fluoride. All of these alternates will have different trace contaminants which will have to be re-qualified by fabs.”

SK Materials began mass producing 15 tons-per-year of ultra-high-purity (UHP) hydrogen fluoride (HF) gas at its in Yeongju, South Korea to support fabs and help reach the government’s goal of 70% local electronic materials supply by 2023. South Korea’s imports from Japan have been replaced to a great extent by an increase in imports from China and Taiwan.

In China, Wengfu has four plants producing Anhydrous-HF (AHF) from FSA, with a fifth plant due to come onstream by early 2021. The company claims that the total capacity of all five plants will be ~105,000 tons/year AHF produced using this route.

This wet chemical market report covers these suppliers: Arkema, Avantor, BASF, Cabot Microelectronics/KMG, CF Industries, Dow/DuPont, Eastman, Evonik, GrandiT, Hansoi Chemical, Hubei Sinophorous, Jianghua Microelectronics Materials, Kanto Chemical, Merck/EMD, Mitsubishi Gas Chemical, PeroxyChem, Rudong Zhenfeng Yiyang, Runma Chemicals, SACHEM, SK Materials, Solvey, Suzhou Crystal Clear, Xingfa, Wengfu.

Critical Materials Reports™ and Market Briefings: Specialty Cleaning Report

November 16, 2020

Wet Copper Deposition Materials for ICs and Packages

Both advanced logic and memory growing demand

San Diego, CA, November 16, 2020: TECHCET announces that the global market for wet metal deposition materials including electro-chemical deposition (ECD) and plating (ECP) chemistry blends in 2020 is forecast to be US$63 million. From semiconductor fabrication at wafer-scale in the Front-End Of Line (FEOL) to wafer-level and die-level advanced packaging, specialized copper (Cu) chemistry blends are seeing compound annual growth rates (CAGR) in demand of 11-13% over the period 2019-2024. While on leading-edge logic chips, cobalt (Co) plating is used to make the smallest connections to transistors, as detailed in the latest Critical Materials Report™ (CMR) quarterly update on Metal Chemicals for FEOL & Advanced Packaging.

While 2/3 of chip packing today still uses relatively simple wire-bonding, TECHCET sees demand for advanced packaging—including flip-chip (FC), fan-in wafer-level packaging (FIWLP), fan-out wafer-level packaging (FOWLP), and through-silicon vias (TSV)—to grow at a strong 8.9% compound annual growth rate (CAGR) over the period 2019-2024 (Figure). These advanced packaging interconnects will continue to use plated solder formulations of tin (Sn) and tin-silver (SnAg), while demand for Cu plating chemistry for interconnect “bumps” and re-distribution lines (RDL) is expected at 11% CAGR over the same period.

“While advanced packaging interconnects are adding more value to final system function, improved metal lines are still needed on most advanced IC chips in heterogeneous integration,” explained Terry Francis, TECHCET Director of Technology and Senior Analyst and author of the report. “On-chip copper metal constrains the speed of the densest ICs today, which has led to use of cobalt in the lower metal layers in 10nm-node and smaller logic devices.”

This report covers the following suppliers: Atotech, BASF, Dow/DuPont, Ishihara, MacDermid/Enthone, Materion, Moses Lake, Soulbrain, Shinhao, Uyemura.

Critical Materials Reports™ and Market Briefings: Metal Chemicals Report

November 5, 2020

Refreshing Material Advances for Logic, Memory, and Packaging

5th CMC Conference “After-Hours” Available up to December 11

San Diego, CA, November 5, 2020: How to keep semiconductor fabs supplied with critical materials despite a pandemic and trade wars was discussed by >250 industry experts gathered in virtual space October 21-22 during the 5th annual Critical Materials Council (CMC) Conference. CMC Fab Members and Associate Supplier Members were joined by leading industry analysts, educators, and investors in discussing business and technology trends in the value-chain for advanced packaging, logic, and memory. The “after-hours” virtual conversations will continue through December 11th using the conference app and website, and new people can join in through November 16th.

“There were a lot good topics especially on materials challenges for leading edge technology and heterogeneous integration, global issues on material supplies, and emerging materials development,” commented Dr. Lihong Cao, Director of Engineering and Technical Marketing at ASE, and Session 4 presenter.

This was the first year that a new conference session was dedicated to Advanced Packaging of Heterogeneous Integration using chips from different fabs. Dr. Lauren Link of Intel discussed the need to find ways to integrate more front-end fabrication materials into packaging. The challenge is how to do so in a cost-effective manner, without over-specifying materials and process requirements as shown in the screen-capture (Figure).

While materials revolutions are happening in advanced packaging, materials evolutions are also essential to improve reliability and quality. Dr. Alejo Lifschitz of DuPont showed how the clever addition of a new “Grain Refiner” additive to the company’s chemistry blend allows for electro-chemical deposition (ECD) of copper (Cu) lines that have reliability engineered into the micro-structure. As deposited, the new Cu grains for the package Re-Distribution Layer (RDL) are <0.2 micron in size with >93% in maximum density highly-twinned <111> crystallographic orientation. This makes reflowed Cu RDL lines that are inherently more resistant to corrosion and cracking when subjected to chemical and mechanical stresses in the real world.

Advanced Logic: finFETs and NanoSheets

Fin-based Field Effect Transistors (finFET) in the most minimally-scaled logic chips will soon be replaced with Horizontal Nano-Sheets (HNS) to improve device performance. HNS are Gate All-Around (GAA) CMOS FETs that reduce power-consumption while allowing for simple patterning of different gate-widths so that designers can optimize power:performance trade-offs within the IC layout. However, both evolutionary and revolutionary new manufacturing processes will be needed for commercial fabrication of HNS logic ICs.

The best example of a revolutionary new process that is needed to make HNS ICs is that of the epitaxial (Epi) growth of the layers to make the transistor channels. Pamela Fischer of ASM in presenting on, “Materials Evolution and Challenges in ALD/Epi FEOL,” explained that when growing alternating Epi layers the interface transition thickness directly determines final device performance. The company’s latest Epi tool allows for alternating ~10nm thick layers of silicon (Si) and silicon-germanium (SiGe) to be grown with extremely sharp transitions of just ~0.5nm. This means that the transition happens in ~2 atomic layers of silicon!

Advanced Memory Materials

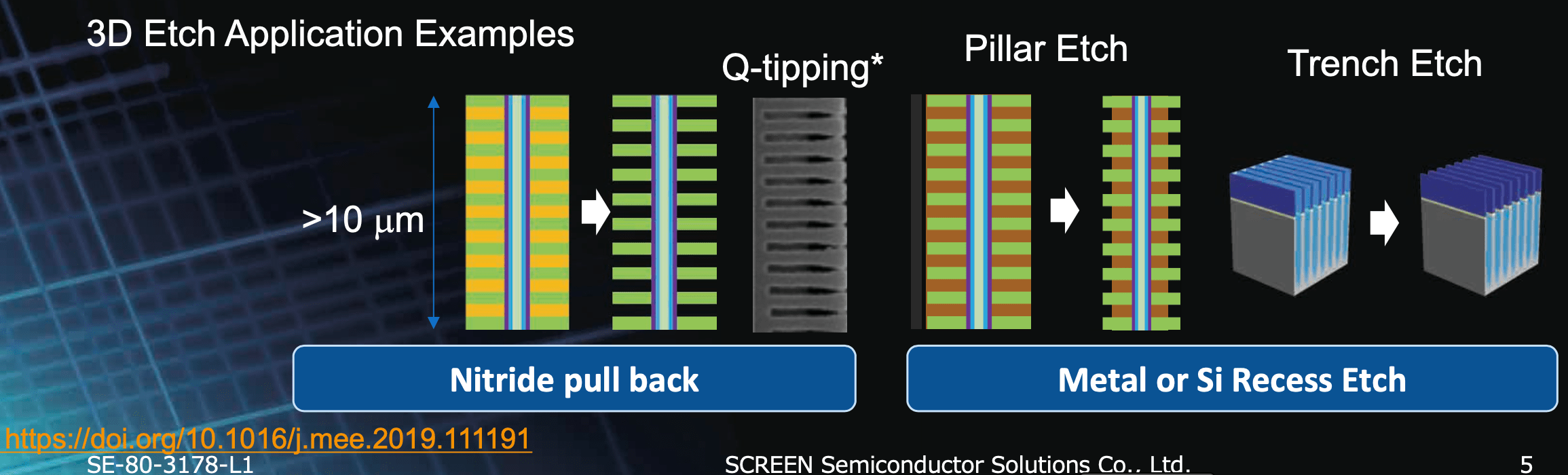

3D device fabrication issues in logic fabs pale in comparison to the ongoing challenges with finding integrated process flows for 3D-NAND memory chips, which currently stack ~100-device-layers and will soon aim for ~200-device-layers on each silicon wafer. Dr. Ian J. Brown, VP Engineering for SCREEN Semiconductor Solutions, showed how “Wet Etching in the 3D Era” has evolved to enable 3D device structures for both logic and memory (Figure). Tools are becoming more sophisticated to allow for chemical blending on-site in the fab, which allows for cost-effective use of more complex chemistry sets. “Digital Wet Etch” (DWE) is a 2-step process similar to Atomic-Layer Etch (ALE), where a first chemistry oxidizes the surface of a metal such as copper (Cu) or cobalt (Co) following which a second chemistry selectively removes just the metal-oxide layer.

Shaun Miller, Director of Global Front End Materials Procurement for Micron Technology, showed why independent regional supply-chains can create, “Material Challenges in Leading-Edge Memory Manufacturing.” For example, differences in supplier infrastructures between the U.S. and Taiwan have led to different levels of metallic and particle impurities in wet chemicals such as sulfuric-acid and hydrogen peroxide, with Taiwan leading in purity at present. Micron is using analytics and “big data” to collaborate on a deeper level with suppliers.

In follow-on conversation, Terry Francis, TECHCET Sr. Analyst who also presented at the conference, explained how hydro-fluoric acid (HF) supply in North America is likely to change in the near term. The raw material supply is changing from mined fluorspar mineral to chemically-engineered fluorosilicate-acid (FSA), since the latter is in surplus as a byproduct of phosphate-based fertilizer production. While electronics manufacturing consumes at most 1% of industrial demand, there is insufficient volume to sustain a supply-chain independent of that for general industry. Such a change in upstream material source would inherently change the trace contaminants in the final downstream HF, which could trigger random yield losses in advanced IC fabs unless materials are carefully re-qualified.

Post-event registration is open until November 16th, so click through to access recordings of presentations and discussions, connect with attendees, and engage in follow-up Q&A!

October 21, 2020

Critical Materials – PVD Targets US$1B and Growing Strong

Increasing demand forecasted through 2024

San Diego, CA, October 21, 2020: TECHCET—the electronic materials advisory firm providing business and technology information—announces that the global market for Physical Vapor Deposition (PVD) including Sputtering consumable materials in semiconductor manufacturing is expected to total over US$1 billion this year. Demand was strong in the first half of 2020 as fabs built up safety stock in response to COVID-19, and sales momentum continued into the third quarter. 2020 revenues are forecasted to be up 2.1% with even stronger growth in 2021 of 5.9% year-over-year, as detailed in the latest Critical Materials Report™ (CMR) quarterly update on Sputter Targets (see Figure).

“The top five suppliers of non-precious-metal targets control approximately ninety percent of the global market,” explained Dr. Dan P. Tracy, TECHCET Sr. Director of Market Research and author of the report. “This mature materials value-chain supports the world’s needs for on-chip metal interconnects, and TECHCET expects that some consolidation in the market is likely over the next several years through mergers and acquisitions.”

TECHCET sees a long-term trend towards recycling of most metal targets to become an increasingly important part of life cycle management. While precious metals such as gold (Au) and Rare Earth Elements (REE) have always been recycled as much as possible, there are both short-term economic incentives as well as long-term sustainability motivations to recycle copper (Cu), tantalum (Ta), and titanium (Ti).

This report covers the following suppliers: Furuya Metals, GO Element, Grikin, Honeywell, JX Nippon, KFMI, Materion, Pioneer Materials, Praxair/Linde, Sumitomo, Tanaka, Top Metal Materials, Tosoh SMD, Solar Applied Materials Technology, Umicore, VEM, and Vital Materials.

Critical Materials Reports and Market Briefings: TECHCET Shop

5th Annual CMC Conference this week: CMC Events

September 21, 2020

Semiconductor Materials Market to Hit $50B in 2020 Up 3%

Winds Reverse on the Global Supply-Chain Seas

San Diego, CA, September 21, 2020: TECHCET announces that 2020 global materials revenues in semiconductor fabrication are now forecasted upward year-over-year (YoY) despite potential disruptions to manufacturing:

• Overall revenues +2.8% to hit over $50B, versus outlook in April for -3%, • Front End Materials +5% to hit $16.4B, and • Equipment Components +10% to hit $3.8B.

While the impact of COVID-19 on the global economy is serious, IC fabrication is steady for devices to Work From Home (WFH) and School From Home (SFH). As predicted, leading-edge ICs to build out data centers are in strong demand this year, as part of forecasted 5.4% Compound Annual Growth Rate (CAGR) for fab materials through the year 2024 (Figure below).

“TECHCET now sees Front-End Materials volumes and revenues for the year 2020 to be buoyed up by cloud computing and devices to support Work From Home and School From Home,” remarked Lita Shon-Roy, TECHCET President and CEO. “In recent online meetings, the members of the Critical Materials Council of Semiconductor Fabricators have said that most fabs are running at normal levels, while leading-edge logic and memory fabs are actually having a great year.”

Advanced logic fabrication now drives a massive 30% YoY increase in demand for cobalt (Co) deposition precursors. Because of the need for speed and reliability in the most advanced finFET logic chips, the smallest on-chip wires are being converted to cobalt from copper (Cu). Interconnect metallization for semiconductors continues to grow in general, so the demand for copper remains strong albeit somewhat reduced. Sourcing cobalt is still problematic due to conflict-mining in the Democratic Republic of the Congo, yet companies such as Umicore and Australian Mines have gone to great lengths to ensure their sources are conflict-free and sustainable.

Chemical-Mechanical Planarization (CMP) Pad Conditioner revenues for 300mm wafers are growing at 4.5% for 2020, due to 3D-NAND device volume growth and overall equipment sales. CMP processing flattens the surface as device layers are stacked up, and the CMP pad lifetime is increased with corresponding manufacturing cost-reduction by use of specialized diamond-abrasive conditioning disks.

Packaging materials revenues for 2020 should be up >1% due to the relative increase in value of advanced packaging, as more and more chips require interconnects faster than wire-bonds. This is a continuance of the multi-year trend of multi-chip packages using flip-chips and interposers and embedded-bridges. Deep details on packaging materials can be found in the “Global Semiconductor Packaging Materials Outlook” report published by SEMI, TECHCET, and TechSearch, available at the SEMI website.

Critical Materials Reports and Market Briefings: TECHCET Shop

To register for 2020 CMC Conference: CMC Events

August 27, 2020

CMP Consumables US$2.5B in 2020 for IC Fabs

Stable world-wide growth in demand forecasted through 2024

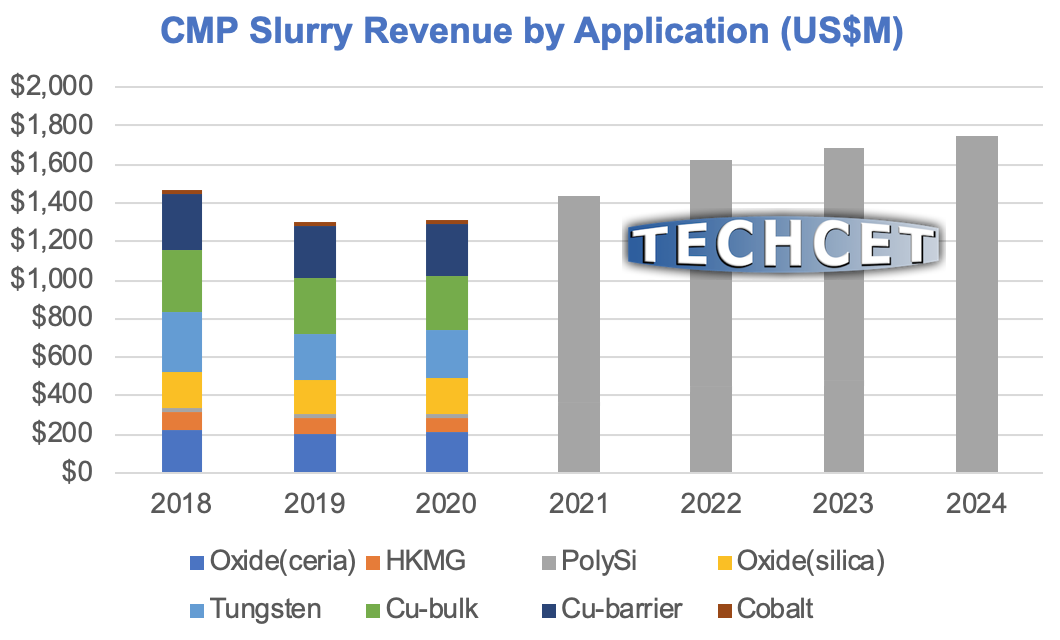

San Diego, CA, August 27, 2020: TECHCET—the electronic materials advisory firm providing business and technology information—announces that the global market for chemical-mechanical planarization (CMP) consumable materials in semiconductor manufacturing is expected to total over US$2.5 billion this year. CMP consumables including slurries, pads, and conditioning disks are all in stable supply globally, despite COVID-19 pandemic disruptions. The total sub-market just for CMP slurries is forecast to be US$1.3 billion this year, with a Compound Annual Growth Rate (CAGR) of 6.2% per year over the period 2020-2024, as shown in the figure from TECHCET’s 2020 CMP Consumables: Slurry, Pads, and Conditioning Disks Markets for Semiconductor Applications report (below).

While the 2020 CMP slurry market will be down ~2.2% from 2019 levels, ongoing demand for both logic and memory IC fabs is expected to drive steady growth through 2024. For logic chips, the largest demand segments are for copper-bulk, copper-barrier, tungsten, and shallow trench isolation (STI), while slurries for HKMG and cobalt are highly value-added despite relatively lower volume demands. For memory chips, increases in the number of layers in 3D-NAND chips drives continued rapid growth in demand for tungsten slurry as well as ceria slurry for high-rate oxide planarization steps.

“Showa Denko’s recent acquisition of Hitachi Chemical was another sign of a maturing semiconductor materials supply-chain,” commented Dr. Diane Scott, TECHCET Analyst and co-author of the report. “This business unit is the world’s leader in supplying ceria slurry, a highly specialized formulation using Rare Earth Oxide nanoparticles to make ultra-smooth surfaces for the world’s most advanced ICs.”

The CMP consumables market is seeing increased focus on localization of the supplychain, with many suppliers looking at finishing product closer to the end-users. Finishing refers to final production steps of the material, which in the case of pads could include application of adhesives, cleaning, quality control (QC) inspections, and specialized clean packaging for shipment. Benefits include reduced shipping cost, faster customization, and localized buffer-inventory to support demand surges.

Critical Materials Reports and Market Briefings: TECHCET Shop

July 29, 2020

Rare Earth Elements Supply Uncertain for IC Fabs

China’s de facto monopoly control remains for now

San Diego, CA, July 29, 2020: TECHCET—the electronic materials advisory firm providing business and technology information—announces supply-chain challenges ahead for Rare Earth Elements (REE) for semiconductor device manufacturing, due to ongoing global pandemics and trade-wars. The United States is fast-tracking domestic REE refining capability to provide a global alternative to China’s current de facto monopoly, but it could be 2022 or later before new capacity is available. The global supply of Rare Earth Oxides (REO) is expected to see a Compound Annual Growth Rate (CAGR) of 4.0% per year over the period 2018-2025, as shown in the figure from TECHCET’s 2020 Rare Earths Supply-Chain Report (below).

“Although China is the global market leader for Rare Earth metals, they do not control all the mining in the world,” commented Terry Francis, TECHCET Analyst and author of the report. “By specializing in the difficult refining and separation processes, Chinese companies have maintained a near-monopoly on rare earth metals production. They own most off-take from global mines such that they ship over 83% of the world’s pure rare earth metals.”

TECHCET is tracking three new REE refining operations in the U.S.:

• Lynas Corporation of Australia and Blue Line Corporation in Texas were awarded grants in late July 2020 by the U.S. government to develop a processing plant to extract rare earths from material sent from Malaysia.

• MP Materials will go public in 4Q20 on the New York Stock Exchange at a valuation of US$1.47B where it will trade as “MP.” The company plans to invest US$489M in refining capacity in Mountain Top, California. In April 2020, the U.S. Department of Defense awarded MP a grant to pay for the design of a heavy REE separation facility.

• USA Rare Earth and Texas Mineral Resources started a heavy and light REE refining pilot plant in Wheat Ridge Colorado last December. It is working on a fullscale refinery for REE, lithium and other technology metals in Round Top, Texas.

U.S. refineries are not expected to be capable of volume supply until 2022 or later. In the meantime, China’s REE companies will control the market. China’s government recently announced a 6.6% increase in quota limits on exported volumes for 2020 over 2019. This is good news for REE buyers, but for new suppliers in the U.S. and Australia it likely means that market pricing will not follow traditional supply-demand trends. Pricing is likely to be highly variable, with possibilities of spikes in the spot market.

Another important market factor is that the handling of rare earth waste is challenging. Countries that are considering local refining capabilities must mitigate environmental risks. For example, USA Rare Earths recently announced their intention to rely on renewable energy for all of their power requirements as one way to balance environmental impacts. TECHCET anticipates more announcements inside and outside of China will be made over the next year addressing environmental concerns.

Critical Materials Reports and Market Briefings: TECHCET Shop

July 4, 2020

Quartz Parts Market for Semiconductor Fabs Downward Trend Expected to US$1.2B

Skilled Labor Shortage for Quartz Tube Fabricator Concerns

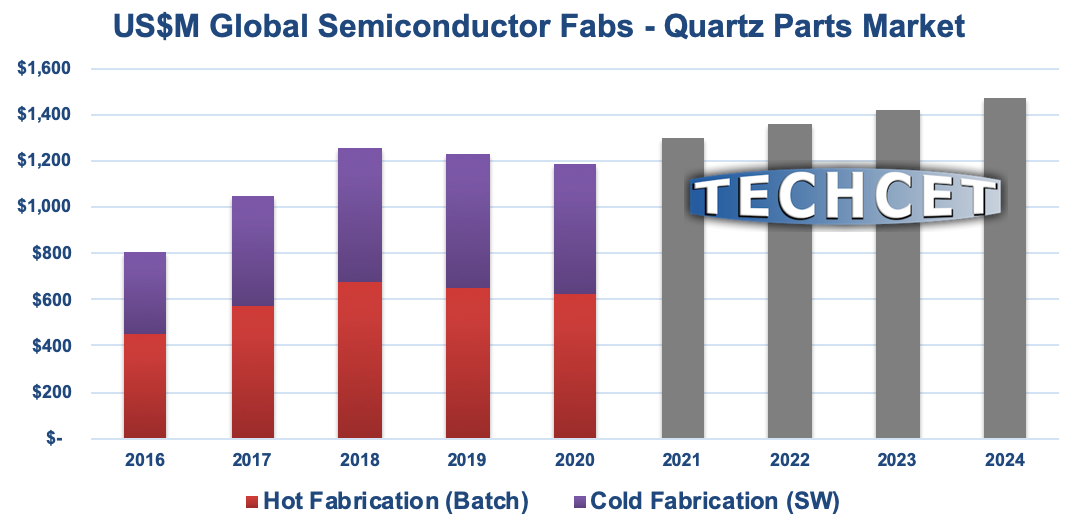

San Diego, CA, July 4, 2020: TECHCET—the electronic materials advisory firm providing business and technology information—announces that the market for quartz components and parts used in Original Equipment Manufacturers (OEM) tools is now forecasted to decline 3-5% in 2020 to reach US$1,187M. However, this market is still expected to experience a 4% CAGR from 2019 to 2024 as shown in the figure.

Other highlights from the 2020 Critical Materials Report (CMR) on Quartz Components, Fabricated Parts, and Base Components for Semiconductor Applications include:

• With the COVID-19 pandemic in 1H20, a few large fabs started increasing purchase orders by 15-20% MoM to increase safety-stock levels,

• China’s market experienced mild growth in 2019, since new local suppliers are still climbing a learning curve; only a handful of companies are able to pass qualification as suppliers to top-tier IC fabs,

• Quartz suppliers in Taiwan will generate +15% revenue growth from Taiwan chip fabs which have continuously run throughout 1H20, and

• Although reports of orders in 1Q2020 appear positive, TECHCET expects softening to start occurring in 2H2020 which will effect overall 2020 revenues.

“The global slowdown due to the COVID-19 pandemic is a good time for quartz suppliers to catch up on the talent shortage,” remarked Kuang-Han Ke, TECHCET Analyst and author of the report. “While machined parts capacity can be ramped up easily, quartz diffusion tube supply depends on experienced craftsman and talent. Many of the mid-size quartz fabricators have been able to out-grow the market with strategic hiring.”

During 2018, legacy equipment parts including furnace tubes faced longer lead-times for the second-tier fabs. This was the result of limited hot fabrication production spots taken up to fill orders from larger volume first-tier fabs and OEM equipment demand.

TECHCET sees the hot growth areas for ICs in 2020 to be in foundry logic and memory chips for high-performance computing and ultra-mobiles. Demand for semiconductor quartz components is largely supported by spares sold by local suppliers, though new furnace and etch equipment OEM sales are important market segments.

Critical Materials Reports™ and Market Briefings: TECHCET Shop

July 1, 2020

2020 CMC Conference – State of the Art Virtual Engaging

5th Annual Materials Event Will Happen in “Virtual Space”

San Diego, CA, July 1, 2020: TECHCET and the Critical Materials Council (CMC) announce that the 5th annual CMC Conference will be delivered “live” October 21-22 weaving worldwide-web services into a valuable digital experience, using a state of the art platform for the best in virtual networking.

The 2020 CMC Conference will feature 4 impactful sessions over 2 days with dynamic Q&A, and will also include a suppliers’ poster session, and Materials Action™ roundtables:

I. Global Value-chain Issues, Including Economics and Regulations,

II. Immediate Challenges of Materials & Manufacturing,

III. Emerging Materials in R&D and Pilot Fabrication, and

IV. Heterogeneous / Advanced Packaging Materials (NEW for 2020).

FEATURED KEYNOTE:

Bruce Tufts, VP Of Technology And Director Of Fab Materials Organization, Intel Corp. presenting “Critical Materials Pushing the Limits for Semiconductor Manufacturing”

30 POWERFUL PRESENTATIONS, INCLUDING THE FOLLOWING:

Dan Hutcheson, CEO, VLSI Research

De-Globalization

Scott Jones, Managing Director, KPMG

Is the World is “On sale”? M&A Activity

Ashutosh Misra, Chief Technology Officer, Electronics at Air Liquide

New Gases for Atomic Layer Etching

Kandabara Tapily, PhD, Member of Technical Staff, TEL

Selective Deposition for Advanced Patterning

Register before August 31st at the Early Bird rate, and optionally select “Advisory Alert Access” to tap into insights from CMC Fab Members and CMC Associate Members on ways to mitigate supply-chain disruptions from COVID-19 and trade-wars.

May 29, 2020

CMC COVID-19 Impact Survey Shows Supply-Chain Strength

Pre-registrants for 2020 CMC Conference access COVID-19 Info

May 29, 2020: The Critical Materials Council (CMC) of semiconductor fabricators & suppliers is continuing to work to mitigate potential supply-chain disruptions by conducting surveys and holding virtual workshops. The May survey on COVID-19 impacts indicates that the global supply-chain for critical materials is strong, with two-thirds of suppliers reporting no disruptions. The CMC has now opened attendance at monthly COVID-19 Briefings and Virtual Workshops to pre-registrants for the 2020 CMC Conference, happening October 21-22 in virtual space.

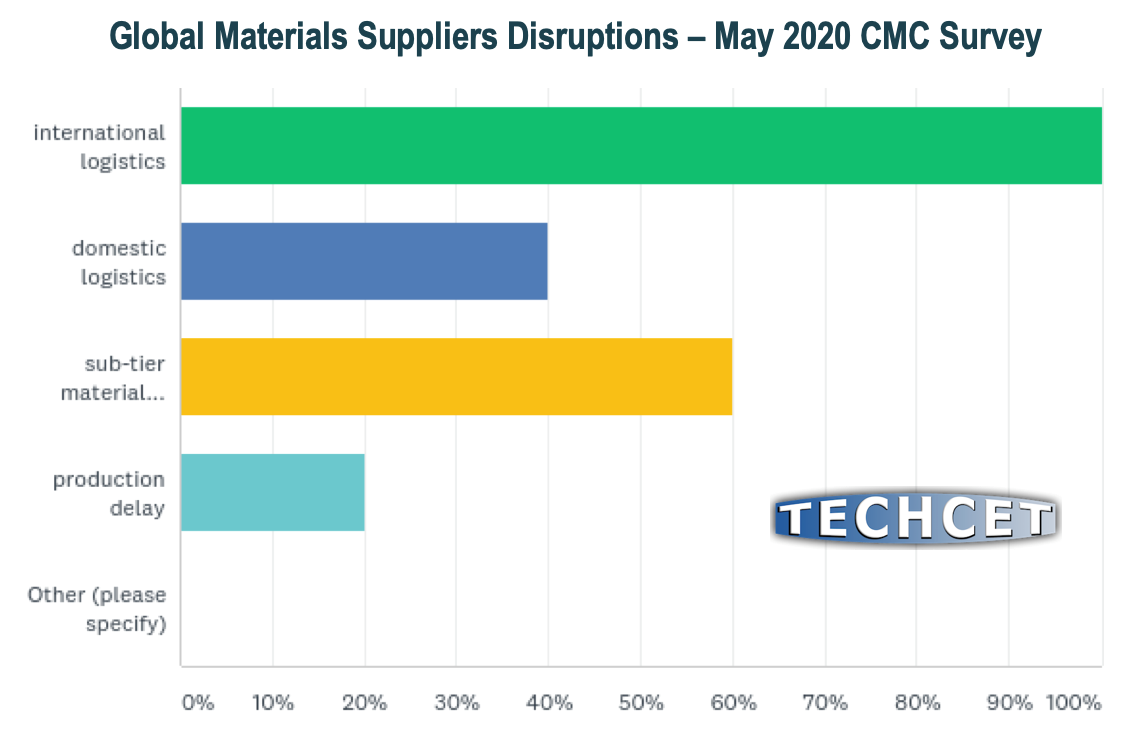

Electronic materials supply companies from around the world responded to this latest CMC survey. About two-thirds of respondents report that they are not currently experiencing any problems with their supply-chains, which reassures fab customers that there should be no disruptions in shipments. However, about one-third (5 respondents) say that there are issues (Figure). Three respondents noted issues with sub-tier suppliers, while two have experienced problems with domestic logistics. TECHCET is tracking renewed interest in establishing parallel local supply-chains for critical materials in all global regions.

The survey shows that 60% of suppliers are increasing their own “safety stock” inventory levels of materials from sub-suppliers. Coincidentally, 60% of suppliers have also restricted all travel by employees, while 20% of suppliers are still traveling to support fab customers. As a strong indicator that the world is now soft-opening from COVID-19 lockdowns, 40% of suppliers now report that customers are visiting their sites, up from 0% in early May. Overall order volumes seem to be the same if not slighter higher than levels one year ago.

BRIEFINGS AND VIRTUAL WORKSHOPS

By pre-registering for the 2020 CMC Conference now, you can attend the next interactive COVID-19 Virtual Workshop on June 24th. These monthly meetings consolidate what is happening now in critical value-chains and provide forecast updates for strategic planning. Pre-registrants will also be able to access news and analysis at the CMC information website.

Daily and weekly analysis at this website on the impact of COVID-19 on semiconductor materials markets and supply-chains includes:

• TECHCET briefings and statistics,

• Global news relating to semiconductor materials,

• CMC Fab Members and Supplier Associate Member survey results, and

• Credible web resources for information on the growing pandemic.

2020 CMC Conference

Featuring a Keynote by Bruce Tufts, VP of Technology and Director of Fab Materials Organization, Intel Corp. on “Critical Materials Pushing the Limits for Semiconductor Manufacturing” the 5th annual CMC Conference will include more than 25 powerful presentations, the popular Materials Action™ roundtables featuring discussions and refreshments, and other networking opportunities.

TNews2

CMC Workshop Flags Looming Shortages of IPA and Sulfuric

Pre-registrants for 2020 CMC Conference access COVID-19 Info

These extraordinary times of greater risks call for more information, so the Critical Materials Council (CMC) of semiconductor fabricators & suppliers is now meeting briefly several times a month to exchange pre-competitive information to mitigate potential supply-chain disruptions. The last meetings exposed a likely shortage in iso-propyl alcohol (IPA) looming just over the business horizon due to the COVID-19 pandemic. The CMC has now opened attendance at monthly COVID-19 Briefings and Virtual Workshops to pre-registrants for the 2020 CMC Conference, happening October 21-22 in Hillsboro, Oregon

Fabs and suppliers say that the supply-chain for semiconductor-grade IPA has the capacity to meet current global requirements (Figure). However, due to COVID-19, governments around the world have mandated that some of the industrial IPA supply-chain be redirected to healthcare and consumer distribution, increasing overall demand. Spot prices for this critical material have reportedly increased a staggering 30% month-over-month (MoM).

Global sources of IPA depend on propene feedstock from oil refiners, and the current economic slowdown has reduced oil demand to such an extent that refineries are being idled. TECHCET has put up “cautionary flags” to watch for 2H20 shortages of IPA and sulfuric acid, as per the latest quarterly update to TECHCET’s Wet Chemicals & Specialty Cleans analysis.

While regional disruptions to IPA supply are nearly certain in the short-term, global materials companies are responding by trying to increase shipments. For example, industry sources indicate that an Asian supplier of IPA is now trying to move material to the US and Europe. In the last COVID-19 Virtual Workshop of the CMC, attendees discussed the ramifications of a reduced number of ships leaving ports around the world, and why they anticipate that the average time to ship cargo will increase.

BRIEFINGS AND VIRTUAL WORKSHOPS

The next COVID-19 Briefing will be given on May 6th, and the next interactive COVID-19 Virtual Workshop will happen on May 27th. Pre-registrants for the 2020 CMC Conference will be able to join in these monthly meetings to learn what is happening now in critical supply-chains, and will also be able to access updated news and analysis archives at the CMC information website. This website (https://criticalmaterials.org/covid-19/) aggregates daily and weekly analysis on the impact of COVID-19 on the semiconductor materials markets and supply-chains. Four folders of

information are provided which include:

-

- • TECHCET Briefings and Statistics,

-

- • Global News relating to semiconductor materials,

-

- • CMC Fab Members and Supplier Associate Member survey results, and

- • Credible web resources for information on the growing pandemic

2020 CMC Conference

Featuring a Keynote by Bruce Tufts, VP of Technology and Director of Fab Materials Organization, Intel Corp. on “Critical Materials Pushing the Limits for Semiconductor Manufacturing” the 5th annual CMC Conference will include more than 25 powerful presentations, the popular Materials Action Roundtables with discussions and refreshments,

and other networking opportunities.

Four impactful presentation sessions will cover:

I. Global Value-chain Issues, Including Economics and Regulations,

II. Immediate Challenges of Materials & Manufacturing,

III. Emerging Materials in R&D and Pilot Fabrication, and

IV. Heterogeneous-Integration / Advanced Packaging Materials.

The fourth session is new for this year, covering system-level performance scaling issues and the materials needed to enable cost-effective “chiplet” packaging. Register for the 2020 CMC Conference now to join the “in crowd” of buyers and suppliers working to keep critical-materials flowing through semiconductor fabrication lines. Know what is happening now, and what risks loom on the business horizon during times of chaos. The next

COVID-19 Briefing will occur on May 6th.

Apr 17, 2020

Choppy Waters for Shipping $50B of Semiconductor Materials in 2020

Risky Sailing on the Global Supply-Chain Seas

San Diego, CA, Apr 17, 2020:TECHCET announces that:

• 2020 global material revenues in semiconductor manufacturing forecasted to decline by 3.0% year-over-year (YoY) despite growth in 1Q2020,

• Impact of COVID-19 pandemic on the global economy is creating choppy waters for shipping and supplying critical materials, as highlighted in recent Critical Materials Council (CMC) monthly meetings, and

• With a return of global economic growth by 2021, compound annual growth rate (CAGR) through 2025 is forecast at 3.5% as shown in the Figure (below).

“From our market research, materials suppliers are increasing production and sales to ensure safety-stock throughout the supply-chain in case there are further disruptions due to COVID-19 cases,” remarked Lita Shon-Roy, TECHCET President and CEO. “Even without further disruptions, we can already see leading economic indicators such as unemployment levels, metal prices and container shipping indices point toward a significant decline in global GDP.” This is supported by the International Monetary Fund’s (IMF’s) current outlook on 2020.

Currently, almost all chip fabs appear to be running at normal levels, with a few exceptions. During this difficult period, YMTC in Wuhan, China reportedly has maintained R&D and grown production of 3D-NAND chips. However, chip fabs in Malaysia report that the government required companies to request permission to continue operating at 50% staffing levels. One company in France had to temporarily reduce production due to their labor union insisting on temporary workforce reductions.

Significant value-added engineered materials including specialty gases, deposition precursors, wet chemicals, chemical-mechanical planarization (CMP) slurries & pads, silicon wafers, PVD/sputtering targets, and photoresists & ancillary materials for lithography are reporting healthy orders and in some cases will see better than expected

revenues for 1Q2020 and April 2020. However, more than 60% of all materials are expected to be negatively impacted before year-end.

Overall demand for commodity materials, such as silane and phosphoric acid, is expected to decline YoY in 2020 by an average of 3% due to softening of the global economy. Average selling prices (ASP) for electronic-grade commodities may drop due to cost reductions in feed-stocks; for example, the global helium (He) gas market which

had been forecasted to be in shortage with high ASPs throughout 2020 has already improved due to COVID-19 slowing down helium demand.

DRAM, 3D-NAND, and MPU chips for server / cloud-computing applications are now in high demand for virtual meetings and remote work. It is yet unclear how much of an increase in materials shipments will be needed to support this segment, however from TECHCET’s modeling of prior cycles it will likely be >7%. Despite such an increase in

the materials used to make leading-edge ICs to build out data centers, shipments in support of legacy node IC fabrication are expected to decline this year.

Consequently, cloud-computing growth may not compensate for overall reduced semiconductor materials demands caused by economic downturns this year. By 2021 the global economy and all chip fabs should return to healthier growth, with materials markets for all IC devices expected to increase at a CAGR of +3.5% through 2025.

Critical Materials Reports™ and Market Briefings: TECHCET Shop

CMC Events: Click here to view all Events

March 9, 2020

EUV Materials Small But Strategic Fraction of $1.6B IC Photoresists Market

San Diego, CA, March 9, 2020: TECHCET announced that the global market for Photoresists and Ancillary Materials declined in 2019 due to semiconductor fabrication market challenges. However, growth is forecasted to resume this year, albeit limited by the COVID-19 drag on the global economy. G-Line/I-Line and DUV photoresists should exceed US$1.6 billion in 2020, as detailed in the latest Critical Materials Report™ (CMR) quarterly update on Photoresists & Ancillaries (see Figure). Meanwhile, the global market for extremely strategic EUV photoresists is expected to be just over US$10 million this year with a compound annual growth rate (CAGR) of over 50% through 2023.

“After many years of delays EUV is finally happening in IC fabrication, with advanced logic lines at Intel this year joining lines at Samsung and TSMC in using EUV, and ASML shipping a new stepper to SK hynix in the fourth quarter of 2019,” explained Ed Korczynski, TECHCET senior analyst and author of the report. “As a clear sign that EUV technology is now ready for commercial manufacturing, specialty EUV resist supplier Inpria just announced a $31 million Series C investment from a syndicate led by photoresist manufacturer and existing investor JSR Corporation.”

Inpria’s new investors included SK hynix Inc. and TSMC Partners. The round also includ-ed participation from existing investors Air Liquide Venture Capital ALIAD, Applied Ven-tures, Intel Capital, and Samsung Venture Investment Corporation.

ASML sold 203 DUV in 2019, and 26 EUV tools with 7 shipped in the third-quarter and 8 shipped in the fourth-quarter. The company claims capacity in 2020 to ship 30 NXE:3400 series steppers, and with anticipated assembly efficiency improvements should be able to ship 40-45 EUV tools per year starting in 2021.

This report covers the following suppliers: Avantor, BASF, Brewer Science, Dongjin Semichem, Dongwu Fine-Chem, DuPont (formerly Dow), Eastman Chemical, FujiFilm, JSR, Kempur, KMG (Cabot Microelectronics), Merck/EMD, Moses Lake Industries, Nissan Chemical, PhiChem, SACHEM, Shin-Etsu, Soulbrain, Sumitomo, Suntific, Tama Chemical, Tokyo Ohka Kogyo, and Versum.

Purchase Reports Here: TECHCET Shop

TNews

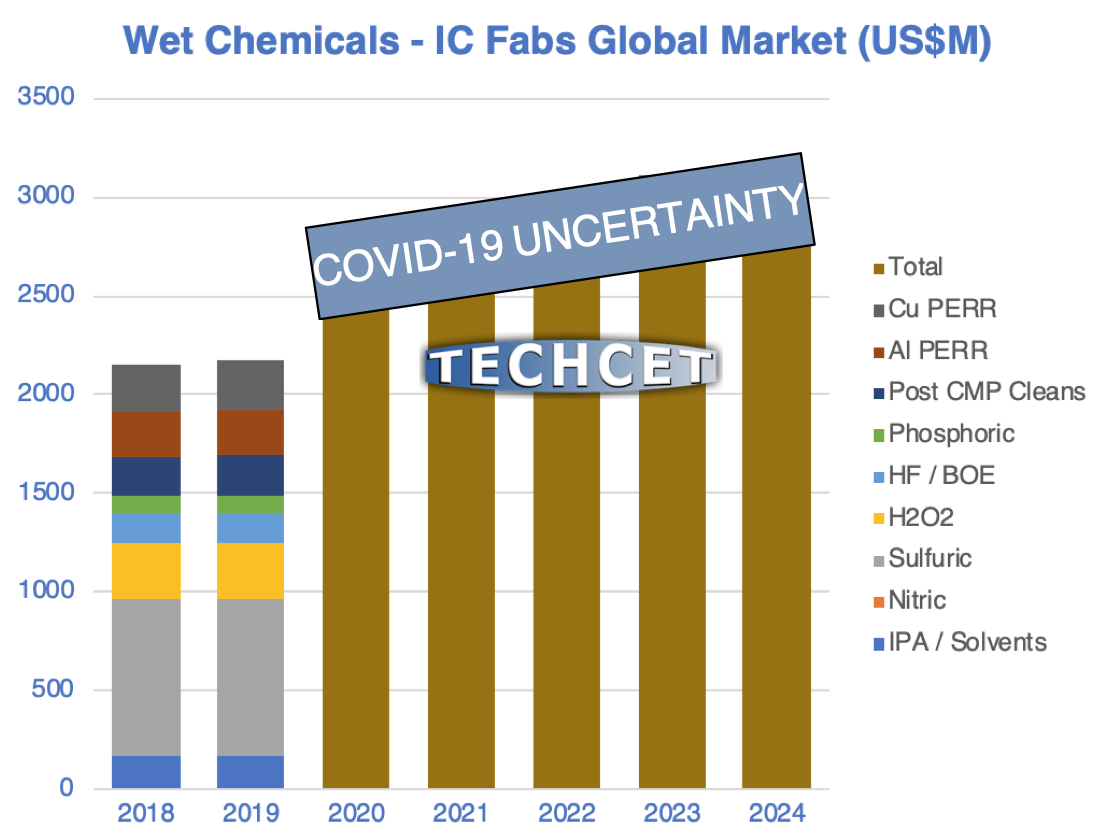

Materials eBlast – Wet Chemicals & Specialty Cleans 2020 Q1

TECHCET announced that Fluorite, needed for hydrofluoric acid (HF), prices in China have decrease by 9% over the last several months. The price situation is dynamic, with China regulators tightening environmental standards resulting in export restrictions and the need to import some raw materials, as detailed in TECHCET’s latest Wet Chemicals & Cleans Quarterly Market Update.

South Korea & Japan have de-Whitelisted each other, thus increasing requirements for exporting to each country. Consequently, South Korea has qualified non-Japan sources of HF gas (for wet chemicals): Befar in China, and Soulbrain and Ram Technology in South Korea.

Chemical specifications continue to change due to greater sensitivity of IC devices at the advanced nodes to impurities. To supply the most advanced fabs, chemical companies must be able to show a “fingerprint profile” of all chemical impurities.

Wet chemicals global market is forecasted to grow from approximately US$2.2B in 2019 to nearly US$2.9B by 2024, with a CAGR of 5.7%, as shown in the figure below:

More info Here

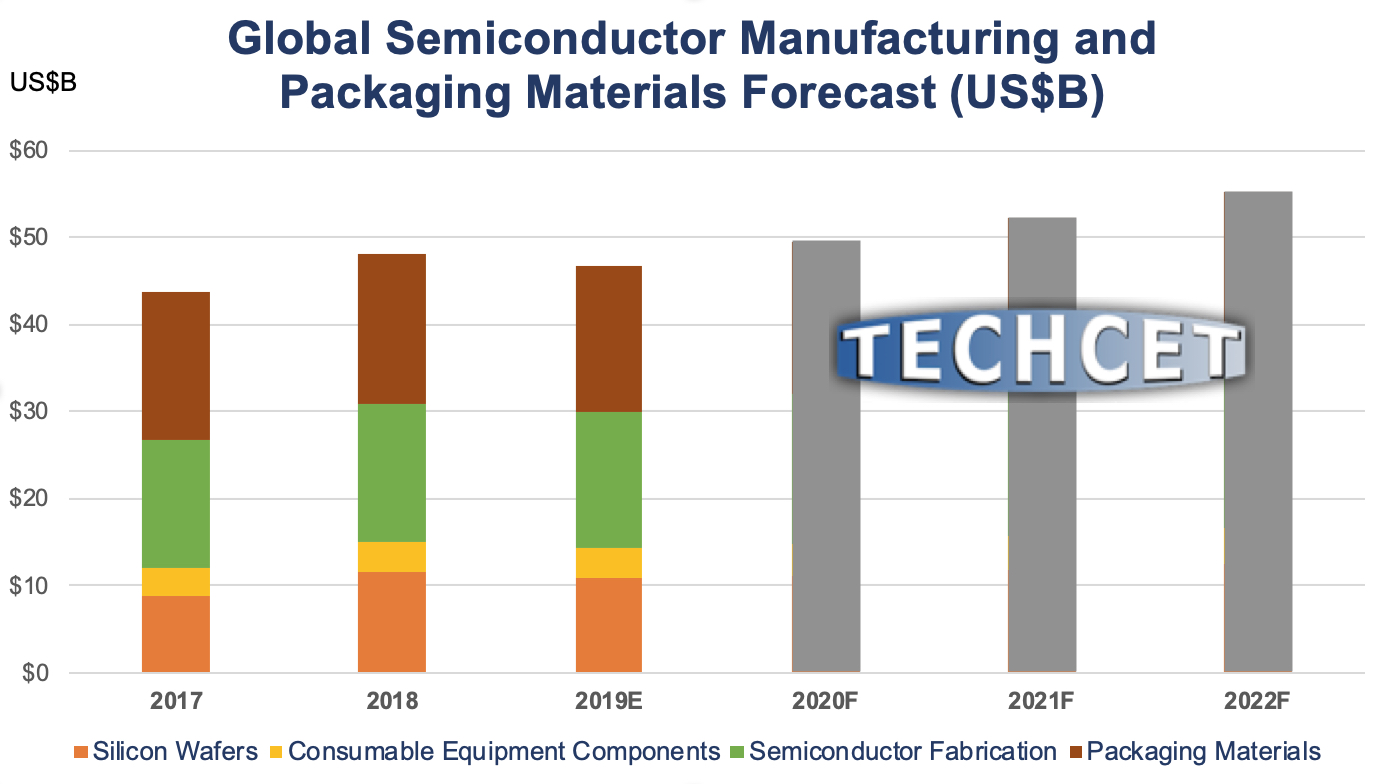

January 14, 2020

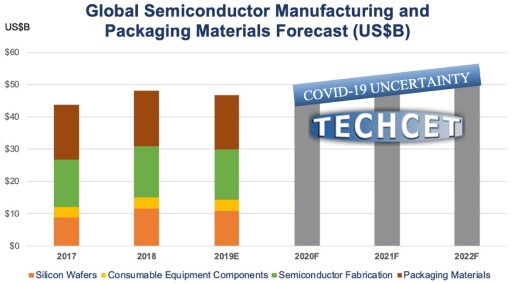

Semiconductor Materials growing to nearly $50B Market in 2020 after Downturn

San Diego, CA, January 14, 2020: TECHCET announced that global revenues for semiconductor manufacturing and packaging materials are expected to grow 5.7% year-over-year (YoY) in 2020 to US$49.5B, of which 65% represents semiconductor fab materials. The memory chip downturn in 2019 reduced total materials market revenues by 2.8% to US$46.8B in 2019, while the compound annual growth rate (CAGR) through 2023 is forecast at 3.5% as detailed in the latest TECHCET Critical Materials Reports (CMR) and shown in the attached figure.

“TECHCET sees the memory sub-market returning to growth in 2020, after the downturn that reduced semiconductor silicon wafer starts by more than 5% in 2019,” said Lita Shon-Roy, TECHCET President and CEO. “The production of semiconductor chips for modern communications, energy, healthcare, and transportation benefits the entire world, so we see steady growth in demand for semiconductor materials moving forward.”

At the 2020 Critical Materials Council (CMC) Seminar—held last October in Taoyuan, Taiwan—representatives of 14 global chip-makers including GlobalFoundries, Intel, Micron, Samsung, and TSMC discussed ways to ensure electronic materials supply-chain robustness in an era of short-sighted protectionist tariffs.

The public 2020 CMC Conference—happening April 23-24, 2020 in Hillsboro, Oregon—will follow private CMC meetings hosted by Intel that week. The keynote address on “Critical Materials Pushing the Limits for Semiconductor Manufacturing,” will be provided by Bruce Tufts, Vice President of Technology and Director of Fab Materials Organization, Intel. A new 4th Session on advanced packaging will highlight materials for chiplets in system-in-package (SiP) devices.

Critical Materials Reports™ and Market Briefings: TECHCET Shop

CMC Events: All CMC Events and Meetings